Blog + News

Commentary & FAQs: Canada Emergency Wage Subsidy (Version April 8, 2020)

On April 1, 2020, the Government of Canada finally released much awaited “details” on the recently announced 75% wage subsidy. Unfortunately, it is clear from what was released that the government still does not have a full grasp of how the subsidy will operate, nor was draft legislation available to demonstrate the operation of the subsidy (as new legislation will be required to implement this subsidy). Along with the announcement, the government released a new name for the 75% subsidy: the “Canada Emergency Wage Subsidy (“CEWS”). CEWS did not replace the old 10% wage subsidy, but rather, was an entirely new program. The CEWS would provide a 75% wage subsidy to “eligible employers” – an entirely new definition which is distinct from the same phrase that is applicable for the 10% wage subsidy – for up to twelve weeks, retroactive to March 15, 2020.

While we are disappointed with many aspects of the CEWS and its rollout, we appreciate the efforts of the government, the Minister of Finance, and the Department of Finance to provide much needed support to the country in this tough and ever-changing circumstances. Our firm – and we know of many others in the tax and business community – stand ready to help the government get it right if they are willing to accept help. This is too important of a moment to get it wrong.

[April 8, 2020 update: the government announced a number of major changes to the CEWS program. This government site contains these updates. Throughout this blog post, we have made updates accordingly.]

A quick overview of what we know about the CEWS program

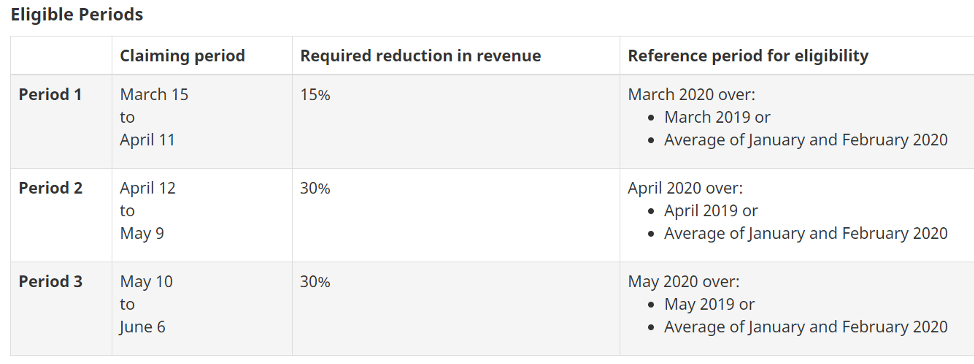

For CEWS, an “eligible employer” includes individuals, taxable corporations, and partnerships consisting of eligible employers (as well as non-profit organizations and registered charities), of all sizes and sectors. In contrast, the 10% wage subsidy, which we discussed here, is only available to Canadian Controlled Private Corporations with more than $nil small business limit, individuals, partnerships, non-profit entities, or registered charities. However, unlike the 10% wage subsidy, in order to be eligible for the CEWS, an eligible employer must have a decline of at least 30% of their revenue compared to the comparable period from the previous year. [April 8, 2020 update: the revenue decline test has been modified to require only a 15% revenue drop in March 2020, but the 30% revenue drop requirement is maintained for April 2020 and May 2020. Also, an alternative benchmarking approach was introduced where an employer may compare their revenue of the month to the average of January and February 2020.]

The below chart provided by the government summarizes the reference period for this revenue decline test, for each of the three claim periods. [Table updated on April 8, 2020]:

The revenue decline test is based on revenue from the employer’s business carried on in Canada earned from arm’s length sources, calculated using the employer’s normal accounting method, and excluding extraordinary items and amounts on accounts of capital. [April 8, 2020 update: the government clarified that the employer may calculate revenue based on either the accrual method or the cash method, but that method must be consistently used for the entire duration of the CEWS program.]

The CEWS is a 75% “subsidy” on wages, but the mechanics of it may operate to actually provide 100% in certain situations where the employee’s current wage has been reduced from the pre-crisis level. According to the details released, the amount of the subsidy will be calculated as follows:

The subsidy amount for a given employee on eligible remuneration paid between March 15 and June 6, 2020 would be the greater of:

-

- 75 per cent of the amount of remuneration paid, up to a maximum benefit of $847 per week; and

- the amount of remuneration paid, up to a maximum benefit of $847 per week or 75 per cent of the employee’s pre-crisis weekly remuneration, whichever is less.

The CEWS application process will be based on self-reporting and attestation. The government announced that it will design anti-abuse rules and introduce harsh penalties (including imprisonment) to discourage mischief. [April 8, 2020 update: If an employer undertakes “artificial transactions” to reduce revenue for the purpose of claiming the CEWS, a 25% penalty will apply in addition to fully repay the improper claim. Additionally, Finance Minister Morneau said that anyone caught taking advantage of the wage subsidy program could face penalties up to 225% of what they’ve received and up to five years in prison.] As shown above, the subsidy will be limited to a maximum of $847 per week per eligible employee for the periods between March 15 and June 6, 2020.

The government also noted that funds will not be available for six weeks, and employers will need to go online via a new Canada Revenue Agency (“CRA”) portal and attest to certain matters (such as the decline in revenue) in order to obtain the funds through direct deposit. This is unlike the 10% subsidy, which is administered simply by the employer reducing its remittance of income tax on payroll withholdings.

[April 8, 2020 update: The government introduced a 100% refund for the employer portion of EI and CPP, with no maximum limit. This is however limited to a very narrow set of circumstances. This refund is only given to employers who are paying employees who are on leave with pay and does not perform any work for the employer.]

As you can imagine, yesterday’s announcement has generated significant questions and confusion. Accordingly, we will address some of the nuances and details of this program using a frequently asked question (FAQ) format. Many of these were actual questions submitted to us. To conclude, we will end by providing our overall comments on the proposed CEWS program.

One caveat: until draft legislation is released, it is important to understand that the actual program may differ from what was announced. Accordingly, stay tuned for more updates. Our answers, therefore, to the FAQs below may change!

FAQs Relating to the Revenue Decline Test

To qualify for CEWS, the employer has to show a 15% decline in revenue in March 2020 and 30% decline in revenue in April and May 2020. What does this mean? [Updated April 8, 2020]

Employers has to apply for the CEWS for each Claim Period.

For remuneration paid during Claim Period 1 (March 15 to April 11, 2020), the employer’s revenue earned during the period March 1 – March 31, 2020 must be 15% less than either:

- Revenue earned during the period March 1 – March 31, 2019, or

- Average of (i) revenue earned during the period January 1 – January 31, 2020, and (ii) revenue earned during the period February 1 – February 29, 2020.

For remuneration paid during Claim Period 2 (April 12 to May 9, 2020), the employer’s revenue earned during the period April 1 – April 30, 2020 must be 30% less than either:

- Revenue earned during the period April 1 – April 30, 2019, or

- Average of (i) revenue earned during the period January 1 – January 31, 2020, and (ii) revenue earned during the period February 1 – February 29, 2020.

For remuneration paid during Claim Period 3 (May 10 to June 6, 2020), the employer’s revenue earned during the period May 1 – May 31, 2020 must be 30% less than either:

- Revenue earned during the period May 1 – May 31, 2019, or

- Average of (i) revenue earned during the period January 1 – January 31, 2020, and (ii) revenue earned during the period February 1 – February 29, 2020.

Given the claim period straddles the reference period, how can employers be sure they will meet the revenue decline test for the month while they are paying their employees during the month? [Updated April 8, 2020]

Good question. Unfortunately, employers won’t know for sure until after the end of the month. For example, the entitlement to CEWS for Claim Period 2 (April 12 to May 9, 2020) is based on whether the 30% revenue decline test is met for the calendar month of April 2020. Therefore, at the time the employer pays its employee for the week of April 12, 2020 the employer cannot be certain it indeed qualifies for CEWS for that wage paid because the 30% revenue decline test is based on the calendar month of April (i.e. April 1 to April 30), which has not ended at that time. This seems problematic and risky for a business owner when deciding whether to keep employees on payroll when they do not know if their business’ future revenue will qualify for the 30% revenue decline test.

Furthermore, employers that engage in artificial transactions to reduce revenue for the purpose of claiming the CEWS would be subject to a penalty equal to 25 per cent of the value of the subsidy claimed, in addition to the requirement to repay in full the subsidy that was improperly claimed.

Does the employer need to submit monthly financial statements with its application each month?

It does not appear so. In applying for the subsidy, an employer would be required to attest that it met the decline in revenue test. The employer is required to keep records demonstrating the reduction in gross revenues and remuneration paid to employees. We anticipate that the CRA will have audit programs after-the-fact to audit CEWS applicants’ eligibility. Employers who were found to be ineligible will be required to repay the CEWS, potentially with penalties and interest.

What does “revenue” mean? [Updated April 8, 2020]

An employer’s revenue for this purpose would be its revenue from its business carried on in Canada earned from arm’s-length sources, calculated using the employer’s “normal accounting method” and would exclude revenues from extraordinary items and amounts on account of capital. Employers are allowed to calculate revenues under the accrual method or the cash method, but not a combination of both.

Special rules apply for registered charities and non-profit organizations.

Is “revenue” profit?

No, revenue means top line / gross revenues under that employer’s normal accounting methods. Expenses should be irrelevant in applying the revenue decline test.

If the employer’s revenue decline turns out to be slightly off what is required under the revenue decline test, is there partial entitlement to CEWS? [Updated April 8, 2020]

No. Based on the rules announced, the revenue decline is an all-or-nothing test. For example, assume the employer has applied for and received CEWS for Claim Period 1 (March 15 to April 11, 2020), and it is later determined by the CRA that its March 2020 revenue was 13% lower than March 2019 revenue, and 14% lower than the average January / February 2020 revenue. Because the 15% reduction is not met on either, the employer will be required to repay all CEWS received in respect of Claim Period 1. Interest and penalties may also apply.

Does the decline in revenue need to be related to COVID-19?

No, nothing in the government’s announcement indicates this as a requirement.

Does the employer have to apply for CEWS every month? [Updated April 8, 2020]

Yes, the employer has to apply for CEWS for each Claim Period. On each application, the employer must attest to meeting the revenue decline test, and report total remunerations paid to arm’s length and non-arm’s length employees during the Claim Period.

Does it matter which accounting standards the employer follows (e.g. IFRS, ASPE, US GAAP, etc.)? [Updated April 8, 2020]

No, it appears that as long as the employer is applying a consistent accounting standard that it had used pre-crisis, it should be considered as its “normal accounting method”. We assume that the purpose of this requirement is to prevent easy manipulation of the 2020 revenue number. In other words, the government does not want employers switching to an accounting method that shows lower revenue for the March to May 2020 periods in order to meet the 30% decline in revenue. If the accounting standard in these months are indeed different than the same months in 2019, be prepared to later explain to the CRA why the accounting standard being employed is the “normal accounting method”.

On April 8, 2020, the government “clarified” that revenues can be calculated under either the accrual or cash method, but not a combination of both. The employer would need to select an accounting method when first applying for the CEWS and would be required to use that method for the entire duration of the program. However, we think this pronouncement is far from clear. We expect that if an employer chooses the cash method of recognizing revenue for the 2020 month, it must calculate the revenues of the comparison month (either the 2019 corresponding month, or the January/February 2020 months) using the same cash method as well. Also, it is not entirely clear whether an employer which had always used the accrual method of accounting would be able to choose the cash method for the revenue decline test – allowing this seems to throw the whole “normal accounting method” requirement out the window.

Is revenue net of bad debts? In other words, if the employer issues an invoice in April 2020 to a customer who refuses to pay, is that invoice amount included in April 2020 even though the employer cannot (and may never) collect? [Updated April 8, 2020]

Warning: although some of the authors are accountants, we have not practiced accounting for years since the sole focus of our work is tax. Our general understanding is that most conventional accounting practices classify uncollectible invoices as an expense item (bad debt expense), and not an offset against revenues. Certainly, if the employer had never reduced its revenues by uncollectible amounts in the past, it cannot do so for March to May 2020 when applying the revenue decline test since that would not be its “normal accounting method”. However, the authors will defer to our accounting colleagues at Moodys Private Client LLP who are actually “real accountants”. 😉

Is this fair? We don’t think so. Perhaps revenues with collection issues should be considered when applying the revenue decline test. Hopefully the government will consider this when it releases the legislation.

Does the April 8, 2020 government statement that the employer has the ability to choose the cash method of recognizing revenue resolve this issue (since revenues not collected would not be recognized under the cash method as revenues in the first place)? As stated in the earlier Q&A, it is not clear to us whether an accrual method employer can simply switch to the cash method. Better guidance from the government is needed.

“Revenue” only includes revenue earned from “arm’s length sources” – what does this mean?

We do not know exactly how the government will legislate this, but if it is based on the definition of “arm’s length” in the income tax context, then an arm’s length person means someone who is not:

- Related to the employer; or

- Factually not dealing at arm’s length with the employer (which typically means they are acting in concert or being directed by a common mind).

For example, an employer corporation’s revenue from a subsidiary it controls, or from a spouse of the owner of the employer corporation, is not revenue from arm’s length sources and would be excluded from the revenue decline test. This becomes an accounting nightmare if a business has never separately kept track of its non-arm’s length revenue (hint: nobody does). There are also many situations where it is unclear if a customer is arm’s length or not, unless a detailed analysis is performed.

We suggest that the legislation contain rules to maintain the arm’s length character of revenue earned from arm’s-length sources, when that income is then transferred within a related group of businesses. This would help prevent disqualification from the CEWS, merely because the payroll entity is not the same as the revenue earning entity. In other words, the fact that a parent – subsidiary structure has been established should not pose an impediment to the employer corporation from qualifying for CEWS. Sometimes, a central payroll entity administers the payroll for the entire group of multiple entities. The central payroll entity charges the other entities in the organization to recover the salary and wages expense paid on behalf of the other entities in the group. In such situation, the “employer” entity only has non-arm’s length revenue and therefore the application of the revenue decline test would be problematic. For situations like this, we will need to wait for the legislation to see how this will be addressed.

The employer’s sole source of revenue is from providing services to a company owned by the father of the owner of the employer. Can the employer qualify for CEWS?

Probably not. The employer has no arm’s length revenue in 2019 and in 2020, so it would not be able to demonstrate a percentage decline in arm’s length source revenue.

How does the revenue decline test work if the employer has both Canadian-sourced revenue and foreign-sourced revenue?

Since revenue for this purpose only includes revenue from the employer’s business carried on in Canada, the revenue decline test should be based on revenues after the foreign-sourced revenue is removed from the months being tested. However, it may be the case that the foreign revenue is actually revenue from a “business carried on in Canada” notwithstanding its foreign source and need not be excluded after all.

We anticipate that as long as a substantial portion of the business activities take place inside Canada, the revenue should be considered to be from a business carried on in Canada (even if the product is sold to a foreign customer). Hopefully, the legislation will clarify this.

The employer had a significant gain in April 2019 from the sale of a building. Is this gain included in revenue in determining whether revenue decreased 30% when comparing April 2019 and April 2020?

For the revenue decline test, revenue excludes amounts on account of capital. This capital gain on the disposition of the building is an amount on account of capital. Therefore, that gain needs to be removed from April 2019 revenue when determining whether revenue has decreased by 30% between April 2019 and April 2020.

The sale of the building in April 2019 may also have caused recapture of capital cost allowance, which is included in income and not on account of capital. This recapture, therefore, would normally be accounted for in the business’s April 2019 gross revenue. It is also possible that the proceeds of sale and recapture in this example would be considered an “extraordinary item”.

We suggest that the eventual legislation deem such recapture to be on account of capital given that the building itself is a capital property of the employer corporation. This example highlights the complexity that some businesses will have in determining eligibility and the complexity the legislation may need in order to create fair eligibility rules.

The employer earned significant revenues in April 2019 due to an extraordinarily lucrative contract it landed. Are such revenues included in determining whether revenue decreased 30% when comparing April 2019 and April 2020?

Probably…for the 30% revenue decline test, revenue excludes “extraordinary items”. Until we have legislation, we do not know what that means. However, under accounting principles, extraordinary items typically mean unusual and infrequent events such as an unexpected natural disaster. Earning significant revenues on a lucrative contract would not likely be considered an extraordinary item under accounting principles. But what if a spike in revenue is caused by a very unusual weather condition? Is that revenue from an extraordinary item and needs to be excluded? Not sure. Legislative guidance is needed.

If the employer did not exist in March, April or May 2019, how would the revenue decline be calculated? [Updated April 8, 2020]

The revenue decline test can be done by comparing the 2020 Claim Period months to the average revenue of January and February 2020. As long as the employer March 2020 revenue is 15% less than the average revenue from the months of January and February 2020, the employer qualifies for CEWS for Claim Period 1. For Claim Period 2 and 3, the employer will have to show 30% decline in revenue in April and May respectively when compared to the average revenue from the months of January and February 2020.

It is unclear how the average January and February 2020 revenue is to be calculated if the employer came into existence during January or February 2020. Also, it appears that if the employer came into existence during March 2020 or later, it cannot qualify for CEWS.

The employer is a start-up established prior to March 2019. It had enjoyed exponential growth since March 2019. Due to the crisis, the employer suffered a 50% decline in revenue from February 2020 to March 2020, but its March 2020 revenue has not declined 15% when compared to March 2019. Does it qualify for CEWS? [Updated April 8, 2020]

Claim Period 1: yes, as long as its revenue from the month of March 2020 is 15% less than the average revenue from the months of January and February 2020.

Claim Period 2 and 3: yes, as long as its revenue from the months of April and May 2020 is 30% less than the average revenue from the months of January and February 2020.

The nature of the employer’s business is such that it invoices its customers annually in December and it has never prepared monthly (or quarterly) financial records. How will the revenue decline test be determined?

We don’t know. It may be based on the yearly revenue divided by the number of months. This could be very problematic because the employer likely has no way of determining what it will be invoicing for the year in December 2020. Alternatively, it may be based on actual work being performed each month – again this is very problematic if the business has never kept monthly accounting records.

How will the revenue decline test be determined if the employer has multiple separate lines of businesses?

Again, we’re not sure. It may require looking at the revenue of each separate line of business, or it may require looking at the consolidated revenues of all businesses. There are many businesses in Canada with very complicated organizational structures. The government will have to design rules that take these complications into account in a fair and appropriate manner.

Existing jurisprudence and CRA guidance in respect of what constitutes a “separate business” is a logical basis to apply the revenue decline test for each separate business. However, how would this affect CEWS eligibility if one business meets the revenue decline test and another separate business within the same employer does not? More guidance is necessary in order to be able to determine eligibility.

For a professional services firm employer that records revenue based on production rather than invoicing, would the revenue decline be based on production? [Updated April 8, 2020]

Since the normal accounting method in this employer is to base revenue on production, the revenue test should be consistent with that approach. It is unclear whether such employer can choose the cash method to calculate revenues for the revenue decline test. If so, revenues will be based on cash collected from clients, and not based on production.

Will financial information provided to substantiate the revenue decline test be used by the CRA to audit other income tax or GST issues?

Probably, if the CRA auditor notices issues worth investigating. The government needs to pay for its stimulus program somehow, so expect CRA audit activities in all areas to increase after the crisis.

What can I do to prepare for the revenue decline test now? [Updated April 8, 2020]

Employers should determine their revenue from income earned from a business carried on in Canada from arm’s length sources (excluding extraordinary items and amounts on account of capital) for each month of March, April, and May 2019. As soon as possible, the determination of the same for January, February, and March 2020 should be completed. We recommend obtaining monthly financial statements for each of the relevant months for 2019 and 2020.

Because it is possible that the government will allow accrual basis accounting employers to use the cash method for the revenue decline test, employers who may not meet the revenue decline test under accrual method may also want to calculate the revenues for these months using the cash basis to see if a more favorable result can be achieved.

It is important to note again that employers should be careful around undertaking measures to intentionally depress revenue to meet the revenue decline test, as a 25% penalty will apply if “artificial transactions” were used to reduce revenue for purpose of qualifying for CEWS.

Other FAQs on CEWS

What is the maximum subsidy under CEWS? [Updated April 8, 2020]

Per employee, the maximum would be $847 per week * 12 weeks (March 15 to June 6, 2020, unless the government extends the program) = $10,164. There is no maximum per employer.

Note that the subsidy is not 75% of $58,700, as commonly referred to in press releases. $58,700 is merely the annualized equivalent of the $847 per week CEWS amount ($58,700 divided by 52 weeks, multiplied by 75% = $847 weekly CEWS).

Under very narrow circumstances, the CEWS program will also provide 100% refund for the employer-portion of CPP and EI, in addition to the $847 per week. This is discussed in a separate Q&A below.

Do employers have to pay the 25% of salary not covered by CEWS?

Unless there was a wage reduction since the crisis for the particular employee, the CEWS is calculated based on salary paid for the week. Therefore, the employer needs to have first paid at least the CEWS, grossed up by 75%, to the employee in order to obtain the CEWS amount. For example, for an employee whose wage is $1,000 per week, the employer has to pay that $1,000 to the employee (with the normal payroll withholdings) and then apply for CEWS of $750. The employer will likely have to attest that it has paid at least the $1,000 of wages to the employee for the week. For situations involving an employee whose wage has been reduced during the crisis, see below.

What is the CEWS amount for an employee whose wages have been reduced during the crisis? [Updated April 8, 2020]

Although somewhat vague, the maximum CEWS for arm’s length employees will generally be the lesser of $847 per week or 75% of the employee’s “pre-crisis” weekly remuneration (but limited by the employee’s actual wage for the week). Pre-crisis weekly remuneration is a calculated amount equal to the average weekly remuneration for that employee between January 1 and March 15, 2020 inclusively, excluding any seven-day periods in respect of which the employee did not receive remuneration.

For example, Employer X has reduced an employee’s wage from $1,200 per week before the crisis to $600 per week during the crisis (or the employee was laid off and hired back at this lower salary after March 15, 2020). Employer X will be entitled to $600 of CEWS for the applicable week. However, Employer X may choose to increase the employee’s wage to $847 per week and be entitled to receive the full $847 per week of CEWS in respect of this employee.

According to the government’s statement, in such situation, Employer X “must make their best effort to top-up employees’ salaries to bring them to pre-crisis level”. It appears some attestation will be required regarding best efforts to pay employees their pre-crisis weekly remuneration, however it is unclear how this will be enforced or how government will determine that a business could have paid its employees more.

Note that there are restrictions on claiming CEWS in a Claim Period in respect of employees who have been without remuneration for more than 14 days. See a later Q&A for details.

Will salaries paid to a non-arm’s length employee be eligible for CEWS? [Updated April 8, 2020]

Yes, however it appears that special rules will be introduced to apply to non-arm’s length remuneration. The backgrounder released states that the subsidy amount for such employees will be limited to the eligible remuneration paid in any pay period between March 15 and June 6, 2020, up to a maximum benefit of $847 per week or 75% of the employee’s pre-crisis weekly remuneration.

The application of this special rule for non-arm’s length employees as compared to the normal rules is not entirely clear to us from the material provided by the government. However, what it appears to suggest is that the CEWS in respect of a non-arm’s length employee will be limited to his/her pre-crisis weekly remuneration, so that a non-arm’s length employee wages cannot be increased after March 15, 2020 in order to increase the employer’s CEWS entitlement. The government did confirm on April 8 that CEWS would not be available for any non-arm’s length employees not employed prior to March 15, 2020, which appears to be consistent with our interpretation of the rules.

Are wages paid to new employees hired during the crisis eligible for CEWS?

Yes. For new employees who were not employees pre-crisis, the CEWS will be 75% of the amount of the weekly wage, up to a maximum benefit of $847 per week.

I laid off many of my employees because I could not afford them, even though there is still some work for them to do. Should I hire them back to work at a rate that is fully subsidized by the government? [Updated April 8, 2020]

As discussed above, the employer can hire the employees back and pay them $847 per week. As long as $847 is less than 75% of the employees’ pre-crisis weekly remuneration, the employer may qualify for CEWS (assuming it meets the revenue decline test) of $847 per week thus covering the entire remuneration.

However, this is still a business decision. The business is still liable for the full payroll costs (including employer portion of CPP and EI), the additional income tax arising from the receipt of the subsidy (which is taxable to the business), and it also would be required to make its “best effort” to top up the employees to their pre-crisis remuneration level. Moreover, the business must have the cashflow to front the full payroll and associated costs before receiving the CEWS which may be many weeks out.

Note that there are restrictions on claiming CEWS in a Claim Period in respect of employees who have been without remuneration for more than 14 days. See a later Q&A for details.

I laid off many of my employees because I could not afford them and I have no work for them to do. Should I hire them back and keep them at home on leave with pay, at a rate that is fully subsidized by the government? [Updated April 8, 2020]

In this case, not only can the weekly remuneration be fully subsidized by CEWS, but the CEWS will also provide a 100% refund for the employer portion of CPP and EI, with no maximum overall limit. To qualify for this refund, the employee must be on leave with pay throughout a week, meaning that the employee is paid by the employer but does not perform any work for the employer throughout the whole week.

The CEWS and the refund of CPP/EI will still be taxable to the employer, and the employer will still be required to make its “best effort” to top up employees to pre-crisis remuneration level. Note that there are restrictions on claiming CEWS in a Claim Period in respect of employees who have been without remuneration for more than 14 days. See a later Q&A for details.

Does the CEWS subsidy apply to contractors?

No. The subsidy will only apply to employee remuneration. In order to remedy this, businesses might be able to terminate existing contractor relationships and hire those contractors back as new employees and obtain the subsidy, provided the business has an existing payroll account (and subject to the other qualification rules including for non-arm’s length employees). Will this be considered abusive? It would seem sensible that if a contractor deals at arm’s length with a corporation, terminating the contractor relationship to replace it with an employment relationship should not be considered abusive. We will await legislative guidance.

Will commissions or bonus income be eligible for the computation of CEWS?

Most remuneration from employment will qualify, including salaries, wages, benefits, commissions and bonuses. Severance pay, employee stock option benefits, and benefits received from the personal use of a corporate vehicle will not qualify.

Can I claim both the 10% subsidy and the CEWS?

Yes, although the amount of the 75% subsidy the employer receives will be reduced by the amount of the 10% subsidy claimed. For timing reasons, we recommend immediate use of the 10% subsidy if you qualify. More specifically, the 10% subsidy is claimed by a reduction in income tax remittance, up to $1,375 per employee and $25,000 for all employees of that business. This can be claimed in the next payroll remittance, whereas the application and the rebate for the 75% subsidy will not be available for at least 3 to 6 weeks.

When will the draft legislation for CEWS be available?

The Department of Finance has said that the draft legislation will be available by the time the application portal is rolled out. Accordingly, we do not know.

How can employers apply for CEWS?

A portal through CRA My Business Account will be developed in the next three to six weeks. Employers should make sure they register for My Business Account and direct deposit with the CRA if they have not already done so in the past. Even if you have previously registered, we encourage trying to log onto My Business Account to ensure you will be ready as soon as the CEWS application process is live:

Is CEWS taxable to the employer recipient?

Yes.

If the employer pays wages to an employee (and applies for CEWS), how does this impact the employee’s ability to claim the Canadian Emergency Response Benefit (CERB)? And vice versa. [Updated April 8, 2020]

To be eligible for the CERB, the employee must involuntarily cease working for reasons related to COVID-19 for at least 14 consecutive days within a four-week period, and must not receive income from employment (amongst certain other types of income) during those consecutive non-working days. Recent government statements suggested that employees with reduced hours (10 hours a week or less) may also qualify too, but details have yet been released. It is clear however that if the employer continues to pay normal wages to an employee throughout the month, the employee cannot qualify for CERB.

If the employee involuntarily ceases to work for reasons related to COVID-19 for at least 14 consecutive days and is not paid wages during those days, the employee qualifies for CERB. However, the employer may not qualify for CEWS for wages that it paid that employee during that Claim Period.

Specifically, here is the rule for employer: CEWS can only be claimed “for employees that have not been without remuneration for more than 14 consecutive days in the eligibility period, i.e. from March 15 to April 11, from April 12 to May 9, and from May 10 to June 6.” If you are scratching your head after reading this, you are not alone. This sentence is not winning any awards for clarity. Let’s use some examples to illustrate this.

Example #1: An employee (Joe) earns wages of $1,000 per week from his employer (Acme Corp). For March 22 to April 4, Acme Corp requested Joe to cease work due to COVID-19 and did not pay him any wages during March 22 to April 4. Joe returns to work on April 5 and is continued to be paid $1,000 per week after April 5. Depending on the employee’s circumstances, Joe should be entitled to claim CERB for the four-week period March 22 to April 18 since he ceased work for at least 14 days.

Acme Corp is now trying to determine if it can claim CEWS for wages paid to Joe in respect of Claim Period 1 (i.e. for wages it paid during March 15 to April 11, 2020). The employee was “without remuneration” for exactly 14 days. Therefore, the employee have not been without remuneration for more than 14 consecutive days from March 15 to April 11, 2020, and Acme Corp should qualify for CEWS for any wages that it paid Joe during Claim Period 1.

Example #2:

Acme Corp has another employee (Lucy) who is in the exact same circumstances as Joe, except that Lucy ceased work during March 21 to April 4 (a total of 15 days). Lucy should be entitled to claim CERB just as Joe did.

In this situation, the employee, Lucy, was without remuneration for 15 days. Therefore, the employee was indeed without remuneration for more than 14 days in the period from March 15 to April 11, 2020. Acme Corp therefore cannot claim CEWS for wages it paid to Lucy during Claim Period 1.

Does this make sense? Not to us. This rule is clearly intended to prevent double-dipping in the CERB and the CEWS system, i.e. that an employee who is eligible for CERB for the month cannot provide the opportunity for his/her employer to claim CEWS on wages paid to that employee after the minimum required 14 days CERB eligibility period. However, based on how this CEWS denial rule is written, both Joe and Lucy were able to claim CERB, but Acme Corp can still claim CEWS for wages it paid Joe simply because Joe ceased work for exactly 14 days. 14 days is the minimum threshold for claiming CERB but one day short of disqualifying the employer from CEWS.

We hope this is a typo by the government, as this rule only makes sense if CEWS were to be denied if the employee is without remuneration for “14 consecutive days or more”, not “at least 14 consecutive days” as it is written now.

Another area of confusion is how this rule applies if the 14 consecutive days straddles the Claim Period. Further legislative guidance is needed.

What happens if the employers make their best effort to determine the CEWS amount, and later it was discovered that they were not eligible? [Updated April 8, 2020]

Employers would be required to repay amounts paid under the CEWS if they do not meet the eligibility requirements. Though no details are provided, we expect arrears interest will be charged on these ineligible CEWS payments. The government will be designing anti-abuse rules, and the government is considering creation of new offenses that will apply to individuals, employers or business administrators who provide false or misleading information to obtain access to this benefit or who misuse any funds obtained under the program. As mentioned above, there is a 25% penalty for artificial revenue depression transactions, and other penalties up to 225% of the improper amount of subsidy received and up to five years in prison.

The CEWS appears very broad and available to all kinds of employers. So, if I understand this correctly, a Canadian professional hockey team – like the Calgary Flames, Edmonton Oilers or the Toronto Maple Leafs – who employs professional athletes might be able to receive CEWS to subsidize their players’ salary?

Yes.

Our Overall Comments

Overall, the announcement made by the government was disappointing. The collective disappointment that we have heard from the overall business community is real. We think it’s fair to say that there was real hope that the government finally realized that the 10% wage subsidy was not enough, and they would get this right with the CEWS. However, yesterday’s announcement – once again – left business owners with fear and uncertainty.

The first major disappointment is confirmation that the government intends to introduce a revenue decline requirement for eligibility. As illustrated, there is no shortage of questions regarding this new eligibility test. Many small businesses – like restaurants and bars who have been forced closed should have no problem meeting that requirement. However, the CEWS will likely have minimal impact on their decision to hire back employees during the period of forced closure. Other businesses will see or are seeing their revenue streams dramatically tightening up while their fixed costs are static. There are many, many businesses who fall into that category and will likely struggle to qualify for the CEWS. Such businesses simply need cash to help them survive. And they need it now. The introduction of such a test would appear to incentivize businesses to have revenue declines rather than encouraging them to retain their employees and protect their revenues to the extent possible. The revenue decline requirement should be eliminated.

That leads to the second major disappointment. The cash from today’s announcement will not be flowing into eligible employers’ bank accounts until at least 6 weeks from now. In today’s world, that is a long time. Too long. Many businesses who do not have cash reserves – and there are many of them – will simply have to lay off their employees or worse yet simply close. There needs to be a better mechanism to put more cash in the hands of affected employers much sooner. For example, what about a hybrid system of the 10% existing wage subsidy? Perhaps eligible employers should be able to calculate their increased rebate, reduce their payroll income tax remittances for the month to that amount and any excess owed to them would be automatically rebated to them through the proposed CEWS system / portal. Anything prohibiting such a system?

The third major disappointment is the administrative requirements that appear to be attached to this program. The CRA portal will apparently not be ready for approximately 3-6 weeks. Again, that is far too long in this environment. The application and attestation requirement will be too burdensome for the average small business owner who may not appreciate the complexities and legal issues associated with attesting that they qualify. For example, does the average business owner understand basic accounting principles such as revenue recognition? No. Accordingly, will they be able to correctly calculate the 15% or 30% decline requirement? Likely not without significant professional accounting help. And if they sign or approve the attestation, will they really understand the negative consequences that can flow from that incorrect attestation? Likely not. This has disaster written all over it.

The fourth major disappointment is the tone that the government has set regarding this subsidy. Numerous times over the last 5 days, either the Finance Minister or the Prime Minister have given stern warnings to Canadians who might want to “game the system” or otherwise make fraudulent claims. It is understandable why they would want to warn such unethical people or fraudsters about attempting to take advantage of a quickly designed system where a “high degree of trust” will be involved. However, such warnings came well in advance of providing details about the new wage subsidy program and with no draft legislation for tax practitioners and / or the business community to assess. Such stern warnings are not appropriate when when no details are available.

Further – and this is the bigger concern – there is no shortage of people, including business owners, who are intimidated by “the TaxMan”. When such people hear stern warnings – even before they know what they’re dealing with – about ensuring they “do it right”, this can greatly influence good and honest people to not utilize programs that are intended to actually benefit them. Why? Because they are scared about the consequences of getting it wrong. In our opinion, the government could have delivered the warnings about “gaming the system” in such a fashion that would have been much more empathetic to the concerns of good and honest people who are afraid of the “TaxMan” because they don’t want to get it wrong. Some business owners would much rather take the ultra-conservative route and lay their employees off and / or wind down their businesses. We are already hearing from people who have now made their decision about what to do solely because of these warnings. Not good.

To summarize, we believe much more work needs to be done to get CEWS right…and quick. As we stated in the beginning, our firm and many others in the tax and business community stand ready to help the government get it right if they are willing to accept help.

Related Blogs

Have you ever wondered how much your US citizenship is costing you? Why renouncing could save you hundreds of thousands and open new doors for financial opportunities.

As US expats prepare for another expensive and stressful tax filing season, we’ve compiled a list of...

Looking to make 2024 your last filing year for US taxes? Here’s what you need to do.

In a recent survey, one in five US expats (20%) is considering or planning to renounce their...

Travelling to the US? If you’re a US expat who doesn’t renounce properly, your trip may never get off the ground.

Air travel can be stressful. Rising airfares and hotel costs, flight cancellations, pilot strikes, long security wait...